As highlighted in a previous article, the housing situation in the U.S. still remains relatively bleak. Sales of new homes stand at just about half the roughly 700,000-a-year pace that analysts consider evidence of a healthy market. In addition, home prices are back to levels not seen since late-2002 (based on the Case-Shiller Composite 20 Index).

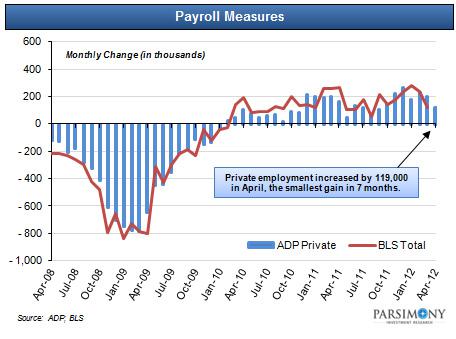

On the jobs front, private employment increased by 119,000 in April, the smallest gain in seven months, after rising by 201,000 in March (according to a report published by ADP on Wednesday).

As shown in the chart above, the ADP report has a strong historical correlation (0.95) with BLS estimates of total nonfarm payroll employment. As such, many analysts now think that Friday's jobs report will come in well below consensus estimates (167,000).

Even if actual payrolls come in close to consensus estimates, monthly employment growth continues to hover below the magic 200,000 number that signals a strong job market. Payroll growth below this level has historically been negative for stocks.

Employment and Stocks

After troughing in mid-2009, monthly payroll growth turned positive again in early 2010 and the job market appeared to be stabilizing (see chart above). The equity market also began to strengthen, rallying significantly throughout 2010 and early 2011.

Payroll growth dropped below 200,000 in May 2011 and stayed below that level for seven consecutive months (through October 2011). As shown in the chart above, the S&P 500 (SPY) was down over 18% from peak to trough over that period.

The Russell 2000 (IWM) fared even worse, declining over 25% over that period (see chart below).

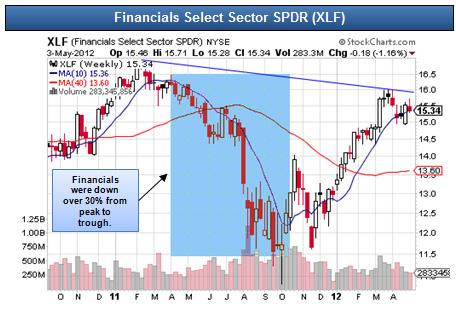

Other high beta sectors like Financials (XLF) and Emerging Markets (EEM) were down over 30% during this sustained period of slow payroll growth (see charts below).

The Tipping Point for Equities?

If the recent payroll report is the start of a new trend of stagnant employment growth, equities could be in trouble in the coming months.

Investors should continue to monitor the employment market very closely and consider hedging their equity positions and/or diversifying into asset classes that will perform better in a "risk off" environment (like precious metals).

As shown in the chart below, gold (GLD) was up over 20% from May 2011 to October 2011.

from seekingalpha

No comments:

Post a Comment